Initiation Report: Mixue Group

A tea drinks juggernaut ready to dominate China and beyond

Introduction

Mixue Group (“Mixue”, “MXG”, or “the Company”; HKEX:2097; market capitalization of US$24 billion) is the world’s largest restaurant chain, serving freshly made tea drinks at over 46,000 locations, primarily in mainland China. Mixue holds a dominant position in the market as a result of its end-to-end supply chain and self procurement efforts that enable the lowest menu prices in the industry. As a result of this approach, Mixue’s revenues, operating profits, store count, cup volumes, and system-level sales are roughly equivalent to all of its tea beverage peers combined, while generating industry-leading EBIT margins and returns on invested capital. The Company is poised to continue growing in a Chinese market that is years away from saturation, while also possessing growth levers in overseas markets and the coffee segment. All of these avenues are supported by favorable consumer trends.

MXG listed on the Hong Kong exchange on March 3, 2025, when the Company sold shares that represented roughly five per cent of shares outstanding. The shares opened up 47% on the date of the IPO, closing at an Enterprise Value multiple of close to 17x EBIT. Shares continued to climb following the IPO, reaching a peak of HK$615.50 on June 4, 2025, equivalent to an EBIT multiple of 38x. We believe this share price appreciation has largely been driven by the tight float available (about 13% of listed shares). Since peaking in June, shares have retraced down 20% to HK$497.80, representing an EBIT multiple of 30x.

While Mixue is expected to grow substantially over the next five years, we believe the Company’s shares are at risk of the multiple falling further to 20x. As a result of this potential outcome, our base case assumptions imply compound annual return of 13% over five years, or 1.7x cash-on-cash, figures that are below our return hurdle of 20%. As such we do not recommend initiating a position at current levels but would revisit the position if we either: 1) gained greater confidence in Mixue’s terminal growth rate to justify a higher exit multiple, or 2) the Company’s stock sold off another 20% from current levels (or 35% from the all-time high). We believe there’s a 50% chance that the stock may weaken further in the short term as the IPO lock-up period expires in less than two months.

Competitive Moat

Mixue Group is the world’s largest restaurant chain with over 46,000 locations, of which roughly 38,000 are in mainland China, as of December 31, 2024. The Company focuses on freshly made fruit drinks, tea drinks, ice cream and coffee, with most menu items prices around US$1 or RMB6. MXG operates almost entirely through a franchise model, selling ingredients, packaging materials, and equipment to franchisees, and also charging franchise fees to store operators. The Company has two brands, Mixue, selling fruit drinks, tea drinks and ice cream, and Lucky Cup, which sells coffee beverages.

The Company’s competitive moat is best understood as an Ecosystem typology, enabled by MXG’s comprehensive supply chain, spanning procurement, productions, logistics, R&D, and quality control. We will discuss Mixue’s supply chain ecosystem, as well as its emerging Brand moat.

Supply Chain Ecosystem

Mixue buys raw materials directly from suppliers across the world and leverages its size to procure its inputs at prices below industry averages. For example, the Company buys 115,000 tons of lemons annually, the majority of which are sourced from a partner in Anyue, China. After procurement, MXG transforms raw materials into store ready ingredients on over 60 automated production lines at five different sites in China. The company self-produces 100% of its core ingredients and 60% of total ingredients internally, including tea, dairy, fruit, coffee beans, syrups, condiments, packaging materials and store equipment. Additionally, MXG is the only drinks chain in China with a liquid milk production license. After production, the Company utilizes its self-operated warehouse system, with 27 nationwide locations, 3.5 million square feet of space, and highly digitalized operations, to store and transport ingredients to the Company’s 46,000 stores. Final-mile delivery is fulfilled by ~40 local delivery service providers in China.

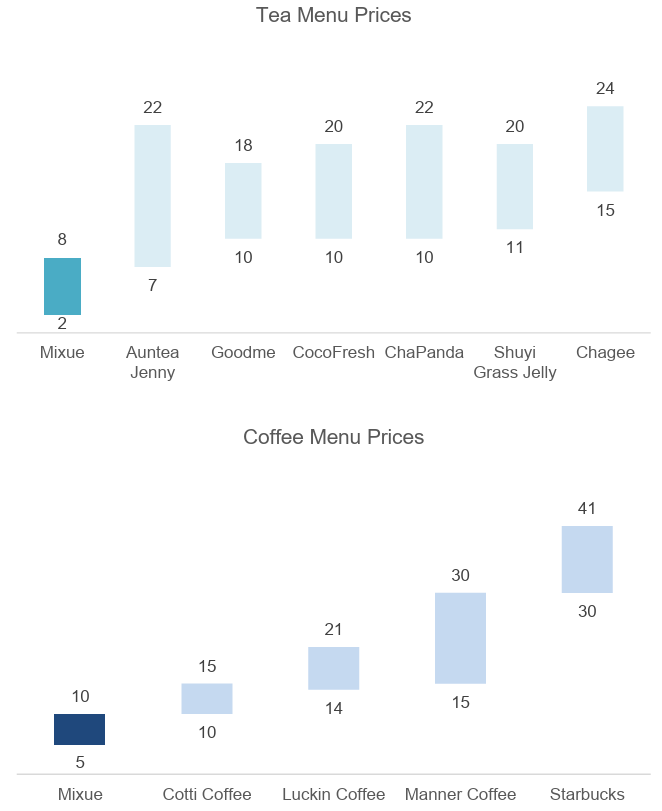

As a result of the Company’s ecosystem, Mixue is able to consistently source and deliver ingredients at much lower costs than its major competitors. For example, MXG is able to deliver lemons and milk powder at costs that are 20%+ and 10% lower than peers, respectively. The final result from a consumer perspective is menu prices that are substantially lower than peers. We summarize the range of menu prices of MXG and its competitors in tea and coffee categories in the following two charts.

Snow King Brand IP

Mixue is attempting to improve the durability of its franchise and further differentiate from its peers by creating brand intellectual property in the form of a cartoon character, Snow King. The character was introduced in 2018, and the Company has produced audio and video content to develop the brand. Hashtags relating to Snow King and the Mixue theme song have been viewed more than 20 and 10 billion times, respectively. In addition, the Company launched a Snow King animated TV show in 2023 that has over 220 million views, and an additional series was released in 2024. Finally, Mixue uses Snow King branding at store locations, in festivals (including an Ice Cream Music Festival), for customers, and also sells Snow King merchandise like toys and water bottles.

Moat Outcomes

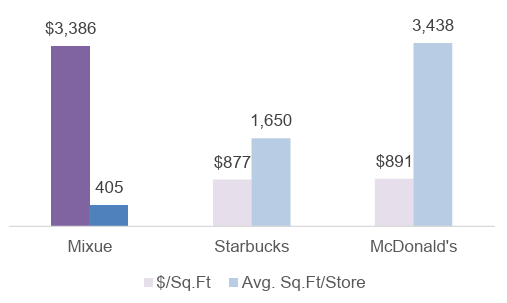

As noted previously, Mixue’s supply chain allows the firm to sell menu items profitably while substantially undercutting competitors prices. These low prices, combined with Mixue’s brand IP results in highly attractive economics for franchise operators. Not only do franchisees benefit from strong demand created by MXG’s ecosystem and IP, they also benefit from some of the lowest up-front and recurring franchisee fees in the segment. Additionally, the median store size is approximately 400 sq. ft, leading to extremely high revenue per square foot, further benefitting franchisee economics. For example, assuming a 1 RMB = 1 USD equivalency (to reflect MXG’s cost base and franchisee perspective), Mixue stores are almost four times more productive than Starbucks stores are. A comparison of average store size and productivity for Mixue, Starbucks, and McDonald’s is as follows.

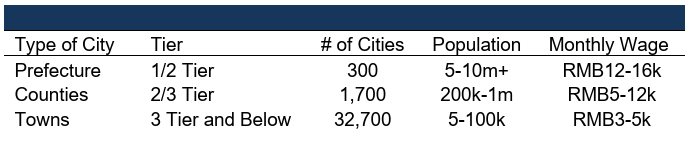

Beyond the franchisee perspective, Mixue’s moat has resulted in one of the largest chain presences in 3rd Tier and lower cities in China. As of December 31, 2024, almost 24,000 (or 57% of the total in China) of the Company’s locations were in 3rd Tier and below cities (defined as cities with populations of 5 million people or less), or more than the next four largest competitors combined. MXG’s presence in these cities exemplifies the strengths of the company, as these cities typically have smaller populations and lower average wages; see below table for an overview of key statistics for the various classifications of cities in China.

Whereas competitors benefit from higher wages and greater population concentration to drive their businesses in 1st and 2nd Tier cities, Mixue’s low-cost procurement and production combine with its extensive distribution network to drive the lowest delivered cost to franchisees in what are comparably remote locations, and at prices better suited to incomes in these regions. In other words, Mixue has a much larger serviceable market relative to its peers as a result of its low-cost supply chain.

Moat Outlook

At present, none of Mixue’s primary competitors (ChaPanda, Goodme/Guming, or Auntea Jenny) possess equivalent supply chains or brand IP. Specifically, MXG has the largest logistics footprint of its peers, as well as the most extensive production facilities. Guming has one processing facility that does not mention specific ingredients, ChaPanda manufactures packaging and tea internally, while Auntea Jenny manufactures tapioca pearls, and tea leaves, among other items at one facility. Additionally, none of these peers possess the buyer power that Mixue does, as system-wide sales at MXG are roughly equivalent to the sum of the aforementioned competitors.

Mixue’s management, as well as the leaders of its competitors have all remarked on a general slowdown in the drinks industry that has combined with intensified competition, putting pressure on per store sales and cups sold. In the short to medium-term basis, we believe that MXG is best positioned to weather this storm, as a result of its size, supply chain, and customer-level economics. Put differently, we see it as extremely difficult for Mixue’s peers to usurp its lead given current industry dynamics.

However, our long-term concern relates to the unproven development of the Company’s brand IP and the resulting ability to establish customer loyalty and pricing power. While there remains some whitespace for the Company’s Mixue brand store count to continue growing in China, we consider it likely that it will reach its saturation point sometime in the next five to seven years. Given how large the Mixue brand store count in China is relative to others (Overseas and Lucky Cup), it will be difficult for MXG to continue growing overall revenues at a meaningful rate unless it’s able to generate same-store-sales (“SSS”) growth at that time. And given the high productivity in terms of the volumes that each store operates at, we see the primary levels for SSS growth coming from 1) price increases, and 2) mix shifts, two changes that may be difficult to achieve when the Company has positioned itself as the lowest cost provider. In other words, our conclusion is that Mixue has yet to elaborate on its strategy to drive SSS growth by delivering more value to customers or demonstrate that its moat produces the price inelasticity that is needed to continue driving growth over the medium to long term.

Strategy

On a go forward basis, there are three major vectors that will drive Mixue’s growth story over the next five years and beyond: 1) growth in China-based Mixue locations, 2) growth in Lucky Cup coffee shops, and 3) growth in Overseas Mixue stores. We will now discuss each in detail

Growth in China-based Mixue locations

Starting at the top, the general thesis for Mixue is that compared to more developed countries, China consumes substantially less freshly made drinks (“FMD”) (compared to packaged or bottled drinks) on both a volume and per capita units basis. As a result, the growing affluence of China’s consumers is expected to drive these figures closer to those of other geographies over time. These figures are provided below.

As a result of the low rates of freshly made drinks consumption, the overall market for FMD in China is expected to grow at roughly 18% until 2028, at which point the sector will represent roughly half of the total drinks market in the country. Importantly, the mass market segment (prices of RMB10 or lower) is expected to growth the fastest and also happens to have the least amount of competition at the time of writing. This data is summarized in the following image.

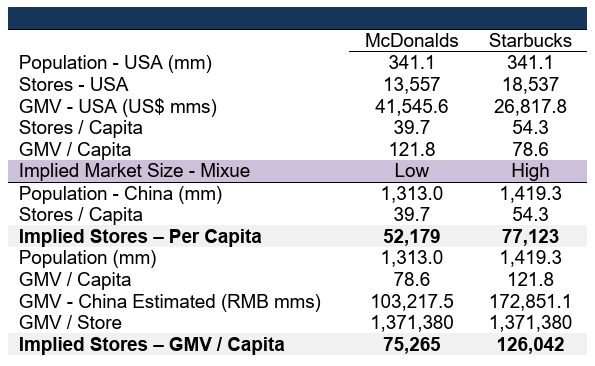

According to this data, the growth story for Mixue is relatively straightforward and robust for the medium term. The question then becomes; how quickly will the Company reach a saturation point for the Chinese market? To answer this question, we took store count data from Starbucks and McDonalds for the US market and compared them to the population of the USA to arrive at a number of stores per capita. We also used system-wide sales (GMV) for both markets to reach a GMV per capita estimate. We then combined China’s population figures for the same period (2024 – although we note that China’s population is expected to decrease by 100 million people by 2050 so have added the latter figure as a conservative estimate in this exercise) and the range of stores per capita to reach a range of implied stores for the Chinese market. We also used these population figures and the GMV / capita from McDonalds and Starbucks to calculate an GMV estimate for Mixue and then divided this figure by the average GMV/ store in Mixue’s system to arrange at another range of implied stores. This latter approach normalizes for Mixue’s smaller store footprint and its higher comparative productivity. Our findings are as follows:

From this analysis, we can see a low estimate of approximately 52,000 Mixue locations in China, an upper limit of 126,000, and a median around 75-77,000 stores. We will refer back to these figures in our valuation section. Finally, we note that these figures apply only to Mixue tea stores. Theoretically, the range of maximum store count for the Lucky Cup brand is equivalent to that for Mixue, and so the hypothetical maximum number of stores for Mixue and Lucky Cup in China would be anywhere from 100,000 locations to 250,000. This simple analysis ignores any relative difference in tastes between Chinese and American consumers, but fortunately only needs to be indicative, given the number of Lucky Cup stores is roughly 4,000 as of December 31, 2024, and so is not at risk of reaching market saturation in the forecast period.

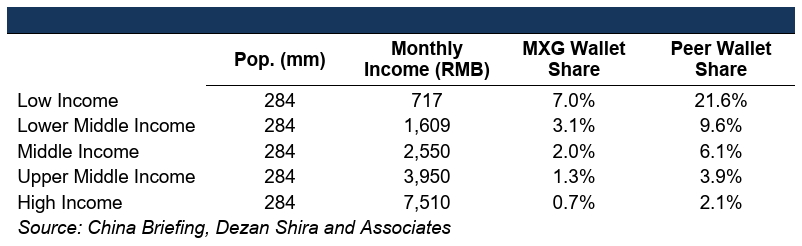

Equally important as our estimates of total store count are the income levels of the Chinese population and how they compare to Mixue’s product offering. For example, if regular consumption of FMD by Chinese consumers was only realistic for a small portion of the market, we would see a smaller implied store count as a result. To analyze the market opportunity from this perspective, we used per capita disposable income[1] segmented by quintile, and then calculated what percentage of monthly income ten drinks at Mixue and its peers would be (average price of RMB5 and RMB~16 respectively). Our results were as follows.

For reference, in the US, the average individual spends between 2.5 and 5% of monthly income on takeout drinks. Given this datapoint, we see that ten drinks per month from Mixue would be affordable by 80% of the population, while less than 60% of the population could afford the same at competitors. In fact, seven Mixue drinks per month would be affordable by all quintiles, based on the average monthly income (although this somewhat overstates the reality given the income figures below the median in the lowest income quintile). Nevertheless, we do not see the income data for China creating a material difference between the Company’s Total Addressable Market and its Serviceable Available Market. Additionally, we see this data as confirming the view that Mixue is well positioned to continue expanding in 3rd Tier and lower markets, while peers will struggle to accomplish the same results given their menu prices.

Growth in Lucky Cup stores

Similar to the tea market, China’s coffee market is also expected to grow rapidly, with above average growth forecasted to occur in 3rd Tier and below cities.

We believe that the same factors positioning Mixue’s tea stores to succeed also apply to its coffee brand, Lucky Cup. These factors include MXG’s supply chain and the resulting low-cost menu items that are affordable to most of the Chinese population. However, the key difference between the two markets is that the Mixue brand is the dominant player in the tea space, while Lucky Cup is attempting to leverage Mixue’s position and supply chain in the tea market to capture share in the coffee market. Lucky Cup is the fifth largest competitor in the coffee market in terms of GMV, and fourth largest in terms of cups sold, or 1.3% and 4% of the market, respectively. In comparison, Luckin Coffee, China’s largest coffee chain (operating primarily through corporate-owned stores) has market share of 22% in GMV terms, and 32% in cups sold terms, while Starbucks has market share of 17% and 8% respectively. However, Lucky Cup’s most expensive item is 30% cheaper than Luckin’s lowest price item, and two thirds cheaper than Starbucks’ least expensive item. At the same time, roughly half of Lucky Cup’s store are in 3rd Tier and below cities, with that figure around 25% and 15% for Luckin and Starbucks.

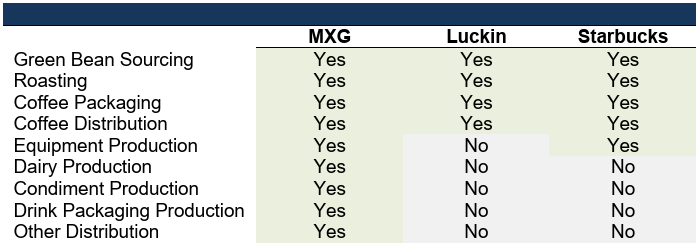

But while Lucky Cup is currently a small player in the coffee market, the Company has a distinct advantage stemming from its supply chain ecosystem that its rivals do not share. Luckin and Starbucks both procure raw coffee beans, roast beans, and distribute beans, but rely on third party suppliers for dairy products, condiments, packaging and the distribution of each. In contrast, Lucky Cup has insourced all of these functions, including store equipment design and production (Starbucks also designs their own equipment but Luckin purchases machines from suppliers). A summary of this value chain position is as follows.

We therefore conclude that Mixue has a reasonable probability (60%) of achieving a sizeable position in China’s coffee market, as a result of its comprehensive supply chain operations and resulting low-cost menu items. However, we believe that the Company must invest in developing additional Brand IP, similar to its approach with Snow King, to effectively compete with the more recognizable brands of its competitors.

Growth in Overseas Mixue stores

The final leg of the Company’s expansion plans rests on its growth into overseas markets, with an initial focus on countries in Southeast Asia. Currently, Mixue has close to 5,000 stores (or 13% of total stores) operating outside of mainland China, primarily in Indonesia and Vietnam. When evaluating countries based on mean disposable income, we find that Indonesia, Vietnam, Malaysia, Thailand, Philippines, and Cambodia have comparable levels to China, and represent 40-50% of China’s population, implying a potential market opportunity of 25-60k stores, or ample whitespace for the forecast period. Mixue’s prospectus notes that the FMD market in SE Asia is more fragmented than China, with a chain penetration rate of 25% vs. 56% in China in 2023, suggesting a more open sandbox for the Company to expand in. Data from the Company also suggests that FMD tea and coffee markets in the region will expand at rate of 20% or faster until 2028.

Even though the market in SE Asia appears more supportive to Mixue’s growth, an overseas expansion does add complexity in the form of investments in the firm’s supply chain. Currently, all of the Company’s production facilities are located in mainland China, with overseas operations supported by a logistics network that covers four countries and 560 cities. Therefore, the Company will need to be thoughtful when expanding production capacity to maintain its product cost advantage while maintaining profitability. The complexity of logistics will also increase dramatically as the firm leverages its production base in China to fulfill demand from a growing number of overseas stores. Given Mixue’s success in China, we believe that management is up to the task but spend some of our time with management trying to understand their approach to developing their supply chain capabilities overseas.

Conclusion

In summary, we believe that Mixue has a truly differentiated business model and competitive moat that position the Company to successfully execute across its three growth levers. We believe further expansion in China has the highest probability of success, and that the Company has penetrated approximately 50% of the market as of December 31, 2024. We conclude that the Company has a tough slog ahead to capture share from incumbents in China’s coffee market but stands ready to outcompete peers as a result of its comprehensive supply chain operations and stands to benefit from a fast-growing coffee market that will act as a rising tide that lifts all boats. Mixue has significant whitespace and a wide-open competitive landscape in Southeast Asia that offers compelling opportunities for growth but will require investments in supply chain and international logistics capabilities to capture market share.

Financial Performance and Benchmarking

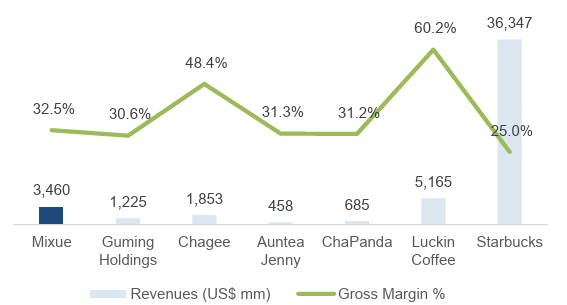

Mixue Group boasts an enviable combination of robust profitability and strong growth, even though the Company is already one of the largest players in China’s FMD sector. In revenue terms, Mixue is almost equivalent to Guming, Chagee, Auntea Jenny, and ChaPanda combined. At the same time, MXG generates gross margins that exceed Guming, Auntea Jenny, and ChaPanda, even while delivering the lowest cost menu items to its consumers. We summarize this data in the following chart.

We note that every peer in the above chart operates primarily under a franchise model, except for Luckin Coffee, which takes a corporate store approach, while Starbucks is a mix of corporate and franchise stores. This observation explains Luckin’s gross margins relative to the rest of the group. We also note Chagee’s margins that lead the franchise only peers and believe this margin performance is explained by the company’s premium position (menu prices of RMB 15-24), limited menu that drives better bargaining power at a lower level of overall cup volumes (consider three products with lower product volumes but with common ingredients that lead to higher aggregate ingredient purchasing volumes compared to ten products that have higher product volumes but minimal ingredient overlap and therefore low individual ingredient purchasing volumes, as an example), and an asset light approach to its supply chain. Deep diving into Chagee a little more, we found that this competitor had substantially higher average GMV per store (RMB6.1m/store is 4.5x higher than the RMB1.4m/store at MXG), and higher RMB/sq.ft (RMB8.1k/sq.ft was 2.4x higher than MXG’s RMB3.4k.sq,ft), suggesting superior store level economics as a result of Chagee’s premium position and higher ASPs. However, when viewed from a cups sold perspective, Chagee stores sold more cups per location in absolute terms, but this was a function of store footprints that are almost twice the size of the average Mixue store; when normalized from a footprint basis, Mixue actually sold about one third more cups per sq.ft, demonstrating MXG’s focus on a volume-driven approach. We also note the material difference in revenues between Starbucks and its Chinese peers, a natural consequence of Starbucks USD-denominated business. If RMB and USD were equivalent (a valid point from a Chinese perspective), Mixue’s revenues would approximate $24B, or roughly two thirds of Starbucks.

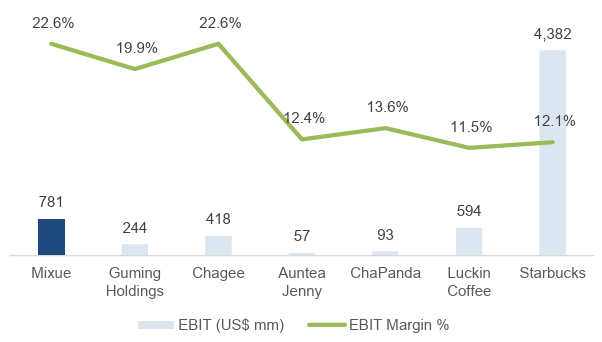

As we shift to an operating profit perspective, the success of MXG’s model emerges dramatically. Even when focusing on the low-end of China’s FMD market, the Company generates industry leading EBIT margins, as well as the highest operating profits in absolute terms. We observe that Mixue’s operating profits are also almost equal to its FMD tea competitors and exceed those of Luckin with revenues that are one third lower. From an RMB/USD equivalent basis, MXG’s operating profits would exceed those of Starbucks. We summarize this data below.

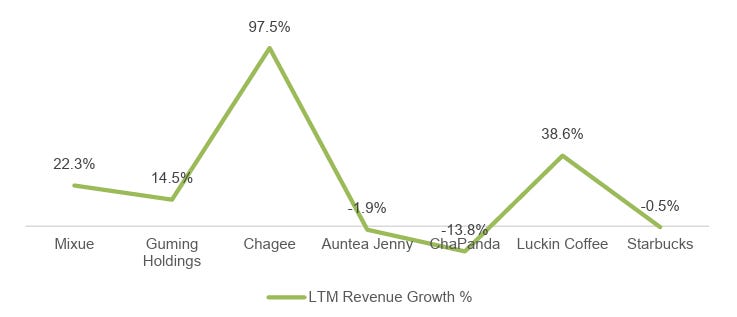

In terms of growth, Mixue trails Chagee and Luckin, but materially exceeds all other competitors. A large driver of the difference in growth rates is simply the law of large numbers. Mixue has more than triple the number of locations as Luckin, and more than seven times that of Chagee. Additionally, the higher menu prices (RMB15-24 for Chagee and RMB14-21 for Luckin) also result in faster revenue growth as stores and volumes scale. LTM revenue growth rates are summarized in the following chart.

From a competitive standpoint, we see Auntea Jenny and ChaPanda’s growth rates reflecting their least favorable positions given the intensifying competition in the market. Chagee’s premium position and low penetration is helping the firm escape the short-term dynamics, while Luckin’s focus on coffee is allowing the firm to generate differentiated revenue growth. We believe that Chagee’s premium position and focus on 1st and 2nd Tier cities will drive higher short term growth at the risk of hitting a saturation point in the Chinese market faster than MXG. On the other hand, Chagee’s differentiated menu, and premium offering may be the most suitable for expansion in developed overseas markets. Guming is the closest proxy to Mixue but may struggle over the medium to longer term given MXG’s scale and supply chain advantages.

Beyond the income statement, Mixue has built a highly cash generative business, with free cash flow as a percentage of EBIT increasing over the past four years to reach 81% in 2024. The Company has been able to convert a higher proportion of operating profits into cash flow by running a negative working capital balance (funded by trade and other payables, likely a function of MXG’s dominant market position) and capital expenditures shrinking as a share of revenues and EBIT. For reference, free cash flow was 18.4% of revenues in 2024 when EBIT margins were 22.6%.

Finally, Mixue has no debt outstanding as of December 31, 2024, and has cash and equivalent balances of RMB 11.1B as of the same date.

Valuation & Expected Returns

To forecast Mixue’s business, we segmented the Company’s store count into Mixue China stores, Mixue Overseas stores, and Lucky Cup stores, and then forecasted each individually, given the differing levels of adoption and expected growth. We then forecasted a GMV per store for each store category; Mixue China and Overseas were assumed to be the same, while Lucky Cup GMV was assumed to be 50% higher based on the mid-point of menu prices compared to Mixue. From there we forecasted Supply Revenue as a percentage of store GMV (or Mixue’s mark-up to franchisees). We also forecasted key COGS items (raw materials, and transportation costs) and operating expenses with sensitivities to all COGS items and material operating expense items: employee compensation for selling and distribution, branding and promotion, and transportation costs for selling and distribution. We summarize our cases as follows:

Base Case

We forecast Mixue China stores to grow at 20% in 2025, slowing to 5% in 2029, leading to 66,000 stores in that period. At the same time, Overseas stores grow at 20% through to 2029, resulting in 12,000 stores at the end of the forecast, while Lucky Cup stores grow 25% in the forecast, also resulting in 12,000 stores in 2029. Our base case assumes flat GMV per store (for all three store segments) given Mixue’s position as a low-cost provider and the resulting need to keep prices low to maintain growth in smaller, lower-income regions in China. We provide a discussion on SSS growth later in this section. The net result is a compound revenue growth rate of almost 17% to 2029, although terminal growth has slowed to 12% from 22% in 2024. We forecast raw material costs to decline by 70 basis points as Mixue leverages its supply chain to further reduce costs. Transportation costs in COGS as a percentage of revenues are flat in the forecast. We forecast employee compensation for selling and distribution to increase 30 basis points to 3% in 2029 as Mixue continues to build out its logistics operations overseas, while branding and promotion expenses rise 30 basis points to 1.5% in the same period as the Company invests in brand IP.

Weak Case

In our weak case, we assume that growth in Mixue China stores reaches saturation earlier with store count growth slowing to 5% in 2028 and 2% in 2029, with close to 60,000 stores in 2029. We forecast a more modest Overseas store growth rate 10%, resulting in ~8,000 stores in 2029, and project a growth rate of 20% for Lucky Cup stores, leading to a store count of almost 10,000. GMV per store assumptions are the same as the base case. We forecast Mixue’s share of GMV to go down by 120 basis points, as competition for franchisees heats up and the Company reduces prices for operators. Revenue growth is 13% over the forecast period, and terminal growth is 6%. Raw material costs go up by 80 basis points due to competition, but gross margins are flat (32.4%) due to D&A leverage. Assumptions for selling and distribution employee compensation are the same as the base case but branding and promotion is assumed to be higher (2% of revenue vs. 1.5%) as are transportation costs (1.4% vs. 1%).

Best Case

Our most optimistic scenario assumes that Mixue China stores continue to grow rapidly, with 75,000 stores at the end of the forecast period, a figure that’s consistent with our median implied store limit for the China market calculated in the Strategy section of this memo. Overseas grows to 24,000 stores (50% YoY from 2025-27 and then 20% thereafter), and Lucky Cup grows to 15,000 stores (30% YoY). GMV per store is flat, but Mixue’s dominance enables it to increase the prices it charges to franchisees, resulting in the Company’s share of system sales increasing 80 bps to 41.5%. Revenue CAGR in this case is 22%, and terminal growth is 17%. MXG’s supply chain enables an aggressive reduction in raw material costs down 130bps to 63%, while achieving modest operating leverage on COGS transportation costs as they drop to 2% (from 2.2%). Mixue also achieves scale benefits for the key selling and distribution expense items: employee compensation (down 20 bps to 2.5%), branding and promotion (down 20bps to 1%), and transportation costs (down 20 bps to 0.7%).

Same Store Sales growth

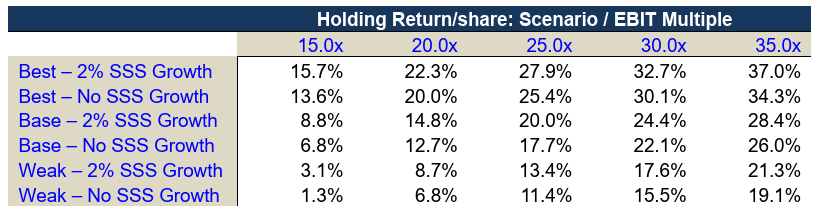

As noted previously, we are cautious around forecasting SSS growth for Mixue stores given the Company’s position as a low-price leader in the category and anticipated growth in lower income geographies. Nonetheless, Mixue does have an opportunity to drive GMV per store growth by introducing new items at higher prices, raising prices on existing items, driving mix shift up in higher income locations, or a combination of these factors. We thus thought it prudent to isolate the impacts of SSS growth relative to the operating scenarios and understand how SSS growth assumptions impacted terminal growth rates and therefore our exit multiple assumptions. We summarize these findings in the following table.

Valuation and Expected Returns

For our valuation and expected return analysis, we opted for an exit multiple based on EBIT. From the peer group, we observed that North American competitors with flat or nominal revenue growth traded at 21-29x EBIT, while the equivalent peer in China (Yum China) traded at 15x. Given our worst cast scenario implies an exit growth rate of 6%, we believe that 20x is the floor for an exit multiple. Assuming a 20x multiple results in an intrinsic value of HK$635.50, suggesting that today’s price of HK$497.80 is a 22% discount from fair value. The same exit multiple implies a 13% compound annual return or 1.7x cash-on-cash for a five-year period. Our sensitivity of returns with each case with no SSS growth, and each case with 2% SSS growth is as follows.

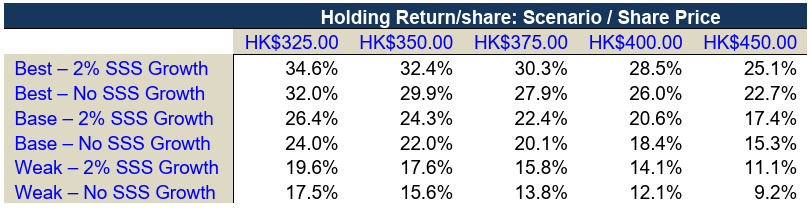

At Mixue’s current price, the Company trades at an EBIT multiple of 28.6x, presenting some risk of a negative multiple rerate at the end of the forecast period. For that reason, our view is that the Company does not confidently pass our hurdle return, even though a permanent loss of capital is very low as forecasted growth would offset a multiple decline. However, we believe the Company would meet our return target if: 1) we gained confidence in MXG’s ability to generate SSS growth, or 2) the Company sold off to ~HK$400 per share. Our sensitivity of expected returns to share price is as follows.

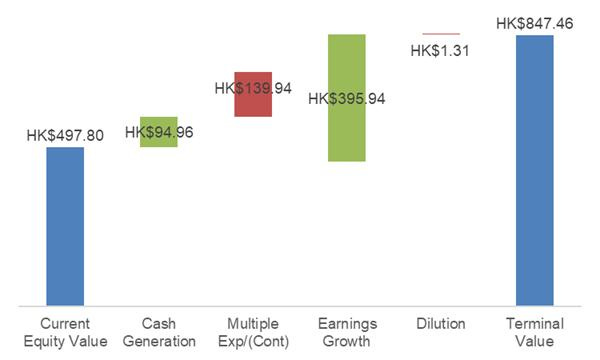

Per the above table, we note that a price of HK$325/share would be a decline of 48% from the Company’s all-time high, but a 27% premium to Mixue’s IPO price. Our view is to wait for a decline of 20% from current levels to start accumulating a position. To conclude this section, we provide a waterfall of the expected return components, assuming our base case with no SSS growth and an exit multiple of 20x.

Management and Execution Capabilities

Mixue was founded by Zhang Hongchao in 1997, who started with a shaved ice store in Zhengzhou, China. After starting various restaurant concepts in different cities, the Company began to formalize its current menu and brand in 2007 when the first franchise store has launched. In the same year, Mr. Zhang’s brother, Hongfu, joined the Company with a focus on front-end operations, such as store management, brand building and product management. After Hongfu joined, Hongchao focused on back-end operations, primarily product development, R&D and the supply chain.

The Zhang brothers are first generation founders that were born to farmer parents and raised in a rural village in Henan province. The Company’s insourcing of ingredients and equipment stems from Hongchao’s early days when capital was tight, and menu ingredients were not available to source off-the-shelf; this DIY ethos formed by necessity has now become institutionalized in Mixue as a firm. The founders’ humble beginnings also influenced their philosophy of winning customers through affordability. Rather than trying to charge customers as much as possible, Hongchao decided to operate on volume, spreading fixed costs as thinly as possible and ensuring quality was higher than competitors. The founders also believe in offering more value to customers to justify higher prices. After reading a short autobiography of Hongfu, we were impressed by the numerous failures that the Zhang brothers overcame in the early days to build Mixue. We believe the founders possess an admirable mix of resilience, curiosity, customer-centricity, a willingness to experiment, and a continuous learning mindset.

As the founders of Mixue, the Zhang brothers collectively hold an 82% economic interest, of which 53% is in unlisted shares of the Company in mainland China. We therefore conclude that the founders and key management personnel are highly aligned with outside shareholders.

Beyond Hongchao and Hongfu, Mixue has two senior executives with material ownership interests, Cai Weimiao (0.2% stake), the head of front-end supply chain, and Sun Jiantao (0.8% stake) who is responsible for business development in Southwest China and Southeast Asia. The Company also counts Shi Peng as chief operating officer, who previously led store and franchise management at Mixue, including standardizing store operating practices. Finally, Zhang Yuan is the Company’s chief financial officer, who previously worked at BofA Securities and Hillhouse Investment. We note that the leaders of Mixue range from 34 years old to 48 years old, providing significant runway for the current team to continue managing the Company.

We were not able to find any documents relating to compensation philosophy or performance targets at this time. We believe this lack of information is mitigated by the incentive of the founders to act in alignment with outside shareholders.

Governance and Shareholder Alignment

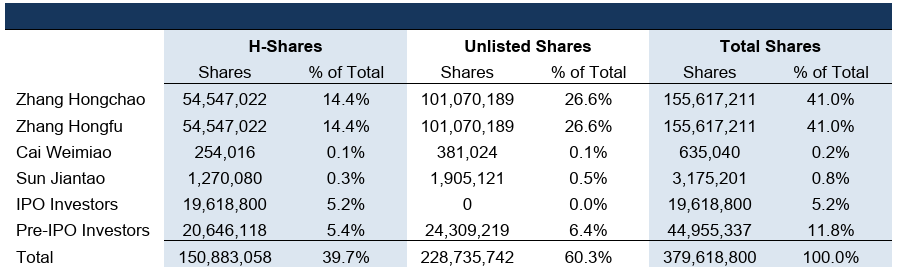

As a result of Mixue’s IPO in March 2025, the Company has two classes of shares: Hong-Kong listed H-shares, and unlisted shares in mainland China. From an economic and voting perspective, the two classes of shares rank equally. However, in terms of legal rights and capital distributions, the H shares have minimal recourse to actions in mainland China and are exposed to potential delays (or non-receipt) of dividend payments from FX controls. We summarize the various shareholders across both classes in the following table.

We note that unlisted shares can convert into H-shares at the holder’s option, but the reverse is not true. While the dual class structure is cause for concern, we believe the sizeable ownership position of the Zhang brothers substantially outweighs any issues that may arise from the structure. We also observe that IPO investors are subject to a six-month lock-up period post IPO (expiring in September 2025), while the Zhang brothers are also subject to six-month lock-up, as well as a further requirement to maintain a controlling interest in Mixue until March 2026.

Even though Hongchao and Hongfu dominate the cap table, the Company’s board structure is overweighted by independent directors relative to the economic interest of third-party investors. Specifically, the two Mr. Zhangs, Ms. Cai, and Mr. Sun hold four board seats, while three (43%) seats are held by independent directors. These directors are Philana Poon, Gary Chu, and Sidney Huang. Ms. Poon has over thirty years of law experience, with practice expertise in M&A, corporate finance, corporate governance, and listing rules, and industry experience in telecom, media, and IT. She is also a director of Meitu, a Hong Kong listed company and has served on three other public company boards in the past. Mr. Chu has over thirty years of experience in the consumer sector, including food and beverage. Mr. Chu was formerly the leader of General Mills’ China business and has led Tiantu Capital’s M&A and buyout department since 2017. Mr. Huang was formerly the CFO of JD.com and currently acts as a senior advisor to the company. Prior to JD.com, Mr. Huang served as a c-suite executive at several China-based technology companies and began his career in investment banking and accounting. Mr. Huang serves on three other boards: Kuaishou Technology (HK-listed), Tuya Inc (dual-listed in Hong Kong and New York), and Yatsen Holding (NYSE listed).

In general, we conclude that shareholders are well aligned with the major shareholders of the Company and believe that board votes are proportionate to economic interests. Even though public shareholders represent a minority of total shareholders, we believe that the board majority is incentivized to act in the benefit of all shareholders given their economic interests in the Company. We also believe the board members of Mixue are well qualified for their roles and should help Mixue broaden its appeal to shareholders outside of Hong Kong and China.

Further Research

To complete our diligence, we would conduct field visits to Mixue’s stores (both Mixue and Lucky Cup) in major cities and more rural areas in China to understand the Company’s offerings from a customer perspective. We would then cross shop Mixue’s stores with visits to its major tea and coffee competitors in China. Finally, we would like to meet with management to ask them a variety of questions to better understand the business and its outlook. Our questions for management would be as follows.

What is Mixue’s plan to drive GMV or SSS growth in the short, medium and long term?

What key obstacles will MXG have to overcome to succeed in the coffee market? What are the key differences in this market compared to the tea market?

What is the Company’s plan for building out its supply chain to support overseas growth?

What does management see as the ceiling for number of locations in China?

If things went to plan over the next five years, what would Mixue look like?

What capabilities do you need to invest in to continue to grow?

What will you have to do differently to keep growing? What will stay the same?

Which competitors do you most respect and why?

Are there any reason why tea shop density in 3rd Tier cities would be lower than in 1st Tier? If yes, why?

How much can store density increase in cities? Counties?

What is the smallest market in population terms that you can address? What about in income terms?

Are there any reasons why FMD in China won’t reach similar levels of consumption as in US/EU/JP?

What is the GMV per store for Mixue China stores, for Mixue Overseas stores and Lucky Cup stores? Please provide the data for each year from 2021 through to 2024.

What is the historical number of Lucky Cup stores?

Please provide detailed financial statements for 2024 that align with the information provided in the prospectus.

What is the split of internal / external sourced supplies and equipment in RMB terms?

What key items are sourced from third parties currently and why? Any plans to insource in the future?

What percentage of total sales are online?

What is Mixue’s value proposition to franchisees vs. competitors?

What is the mark-up at the franchise level?

What is the typical payback period for a new franchisee?

How much do franchisees typically earn?

Have you lost any franchisees to competitors? If yes, why?

Have you won any franchisees from competitors? If yes, why?

Do you keep track of your wins and losses from/to competitors? If yes, what is your win/loss ratio?

What is the usual timeline to open a new store?

How long does it take for a new franchisee to open a store?

How do you find and attract new franchisees?

How do you collect and analyze franchise feedback?

Stores opened in 2023 show weakness in GMV per store relative to other vintages. Why?

We also noted an increased number of franchisee exits in 2023. Why?

Why are franchise fee margins are going up?

Please provide details on your membership program. What are the benefits? Any key statistics to highlight?

Why are there shortfalls in social insurance and housing fund contributions as noted in the prospectus?

[1] https://www.china-briefing.com/news/china-middle-class-growth-policy-and-consumption/