Initiation Report: Kokusai Electric (TSE:6525)

High torque exposure to changes in semiconductor architectures at an attractive valuation

Below is my initiation report dated December 6, 2024 on Kokusai Electric. Since writing the report, I initiated a long position at ¥2,279.50 / share (roughly 10.4x 2025E EBIT), that has now appreciated to ¥3,629 / share as of February 15, 2025 (or 16.5x 25E EBIT). I will provide an update to the story based on Q3 earnings in a subsequent post.

Please reach out if you’re interested in a PDF of the report or the financial model.

Executive Summary

We recommend initiating a position in Kokusai Electric (TSE:6525, or “KE”), the world's leading manufacturer of batch atomic-layer deposition (ALD) equipment. Batch ALD tools are a key enabler of new architectures in logic and advanced memory chips. The company has 70% market share in its segment, which is expected to grow significantly, given a recovery in the wafer fabrication market in 2025, as well as by Process-of-Record (POR) wins as leading chipmakers launch new advanced node semiconductor lines in 2025 and beyond. Kokusai has strong validation of its technology capabilities, as Applied Materials (AMAT), one of the world's largest wafer fabrication equipment (WFE) companies, attempted to acquire the company in 2021 but was blocked due to regulatory concerns and remains a strategic investor.

The company is trading at a significant discount to intrinsic value as a result of KKR's decision to reduce their economic interest in the business by half, following Kokusai's IPO in late 2023, compounded by general weakness in the WFE sector. KKR had acquired the company in 2017 as a spin-off from Hitachi and is now in the process of exiting its investment after a 7-year holding period. KE’s current price of ~¥2,300/share is 60% below its all-time-high of ¥5,850 reached in July 2024. We anticipate a 5-year compound return of 39%, or approx. 4x cash-on-cash, driven by increasing ROIC as the company takes advantage of its newly built manufacturing capacity that will support double-digit revenue growth to 2029.

Competitive Moat

The company is the world’s leading designer and manufacturer of batch, atomic-layer deposition equipment. Deposition is a critical step of the semiconductor chip manufacturing process, where materials, typically metals and oxides, are placed on a wafer to form the transistor, signal, and power layers of a chip. The deposition phase is repeated up to a hundred times on each wafer and requires high precision equipment to place the materials in accordance with the chip’s design specifications.

There are multiple forms of deposition techniques, including electroplating, physical vapor deposition (PVD), chemical vapor deposition (CVD), and ALD. ALD is the most precise method of deposition as it involves depositing a single layer of atoms onto a wafer at a time, resulting in wafers that are free from the defects that other forms of deposition typically produce.

However, ALD has traditionally had very low throughput, as wafers went through the deposition stage one at a time. This is referred to as single-wafer ALD. In comparison, batch ALD processes multiple wafers at a time; anywhere from 10 to 175 per batch. In essence, batch ALD combines the precision of ALD with the throughput benefits of less precise deposition methods. The difficulty in producing batch ALD systems rests in the control of the conditions of a large deposition chamber, as the gas inflow and exhaust venting determines the success of the deposition process. In comparison, single wafer deposition chambers are much smaller than batch deposition chambers, making the former’s environmental conditions easier to control. Without sufficient control of the chamber, the deposition equipment will not produce a wafer in line with its specifications, resulting in low wafer yield for the chip manufacturer.

Kokusai Electric is the clear leader of batch ALD worldwide. The company is estimated to have 70% of market share in the segment, while it’s main competitor, Tokyo Electron, has the remaining 30%. The company has received POR awards from all of the major chipmakers, meaning KE’s tools have been specified for high-volume chip manufacturing lines at various fabrication plants. Furthermore, Applied Materials, one of the world’s largest wafer-fabrication equipment (WFE) manufacturers, with a presence in single-wafer deposition tools, made an offer to buy KE in 2019 for $2.2B, and then raised its offer to $3.5B in 2021 (compared to $3.5B at the time of writing), only for the deal to be rejected by China’s government and ultimately withdrawn by AMAT. We believe that AMAT’s attempted purchase strongly validates KE’s technology leadership in the space, while also demonstrating the difficulty in replicating the technology. We also speculate that the size of the market (ALD is a much smaller subset of the total deposition market; anywhere from 5-10% of the total), combined with KE’s technology lead prevents other larger players from entering the market organically.

In addition to designing and manufacturing batch ALD tools, KE also provides field services to customers that have installed the machines at their fabrication facilities. KE is focused on increasing the service revenues of its business as they grow the installed base of their equipment.

Strategy

In the next several years, the chip-making industry will be disrupted by several innovative new architectures to enable continued density scaling and cost reduction. Specific to the ALD segment, the introduction of 3D memory designs and gate all-around (GAA) transistors in logic chips will increase the usage of ALD in high-volume manufacturing.

3D Memory / DRAM

Generally speaking, chipmakers have reached the limits of their ability to shrink the size of the capacitors in memory chips on a horizontal plane. As a result, the next phase of density scaling requires layering memory chips on top of each other to increase the density of DRAM on a 2D footprint. The following diagram represents this visually.

Due to design innovation, memory chip designs will increasingly be marked by structures with high aspect ratios (HAR). The aspect ratio of a shape is the relationship between the vertical height of a structure and the horizontal width of a structure. For example, a form that’s 5 inches tall by 1 inch wide has an aspect ratio of 5 (5 / 1). Current NAND storage memory structures have aspect ratios of up to 70:1, and it’s expected that DRAM chips will follow suit. KE has already established a dominant presence in the ALD market for NAND memory and will leverage this capability as DRAM chip makers are forced to deploy batch ALD to manufacture 3D DRAM device with HAR structures.

Separate to the innovations in DRAM design, we also see the continued adoption of GPUs in datacenters and AI applications as creating a material tailwind for 3D DRAM. A significant bottleneck in the overall performance of GPUs in AI training and inference is the amount of DRAM memory on a GPU chip. Therefore, as demand for GPU chips increases and the performance of GPUs rise in tandem, there will be a resulting step change in demand for DRAM chips, particularly for 3D DRAM due to its performance benefits.

Gate All-Around transistors in logic

In logic semiconductors (CPUs and GPUs), current FinFET transistor designs cannot shrink any further without impairing the basic functionality of the device. Specifically, further shrinking of FinFET transistors significantly increases the electrical leakage of the transistor when switched off, impairing the basic functioning of a chip. In response, chipmakers are transitioning to GAA transistors that enable continued compute power density improvements without experiencing the electrical leakage issues that plague further miniaturized FinFET designs. Visually, the transition from FinFET to GAA transistors can be seen in the following image:

While the gates in FinFET logic chips appear to have higher aspect ratios than those in GAA, what actually matters is on the inside; each gate (the horizontal “fins”) in a GAA transistor has multiple layers of material inside of it, each of which have multiple HAR surfaces that require ALD tools. In short, the demand for ALD tools will increase in logic chips (which historically have not needed ALD), and volume needs for logic chips will focus that demand on batch ALD processes.

In summary, there are two key innovations in memory and logic chips that will drive increased adoption of batch ALD tools by the world’s leading chipmakers. We note that KE is already serving the largest manufacturers of 3D NAND chips (Samsung, Kioxia, Western Digital, SK Hynix, and Micron), and therefore possesses the skills and capabilities to apply its technology to customers in other chipmaking verticals. Importantly, we note that TSMC, the world’s largest logic chip manufacturer, is already using KE’s batch ALD tools in logic applications; TSMC was KE’s second largest customer at the time of the IPO.

Financial Performance and Benchmarking

As KE’s IPO on the Tokyo Stock Exchange was on October 25, 2023, the company has only provided financial results from FY2022 onwards, limiting our analysis.

However, we note that KE’s most recent fiscal year (ending March 31, 2024) showed a 26% decline in revenues on a YoY basis, driven by overall softness in the semiconductor and WFE sectors. Revenue performance for peers during the same period is as follows: LRXC (-24%), AMAT (-0.5%), ASMI (-2%), TEL (-17%). The company’s relative performance was attributed to its higher exposure to a soft NAND market. While the company’s revenue performance was disappointing, it masked a cyclical recovery, as quarterly revenues bottomed in Q1 and recovered to the extent that Q4 revenues were roughly double those of Q1. Management expected a further recovery in revenues at the time of reporting, which has proven true as the company posted quarterly revenues in Q1 and Q2 for FY25 that were sequentially higher than the prior year periods. At the same time, management has provided optimistic comments regarding a general recovery in the WFE market, and KE’s revenues specifically, commentary that has stood in contrast to continued weakness in the share price over the same period.

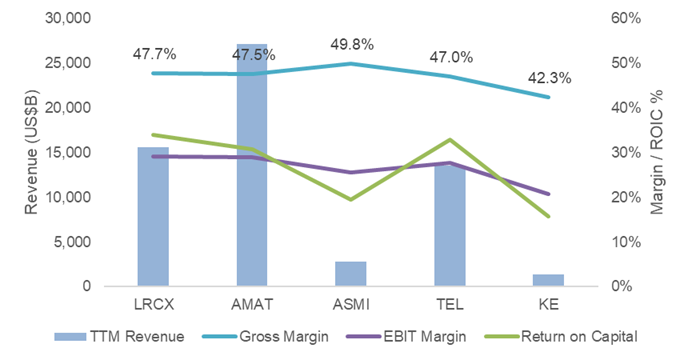

When compared to peers, the company’s performance is relatively weaker, which we ascribe primarily to differences in scale. We summarize TTM revenues, gross and EBIT margins, and ROIC for each company in the following graph:

We note for reference that KE’s revenues are $1.4 billion USD on a TTM basis, compared to $27.2 billion for AMAT, and $2.8 billion for ASMI. Our view is that a gross margin of 42.3% on revenues that are less than 5% of AMAT’s is fairly impressive. The company is also in the process of completing a new manufacturing facility to add capacity and has invested in fixed overhead to grow its business. We therefore expect to see an increase in EBIT and ROIC as the company begins to benefit from the incremental capacity it has built. Assuming the company pays out dividends in line with is stated policy, we expect ROIC to increase to 29% in 2027 (vs. 16% on a TTM basis per CapIQ). On the topic of R&D spend, we observed that the company’s investment rate of 6% of revenues was low relative to peers (range of 3 – 21% of revenues, with a mean and median of 12%). We do not have enough information to judge whether this is artificially low and a forward indicator of a shrinking technology lead, or a result of a defensible market niche. Further diligence on this point will be key point to understand to complete our analysis.

The company has a modest amount of debt. As at fiscal year-end 2024, gross debt was 2.2x EBIT but the company was in a net cash position when accounting for cash balances at the same point in time. The debt has minor principal repayments in 2025 and then requires complete repayment in 2026. All principal repayments can be funded by a combination of cash from operations and existing cash-on-hand.

Valuation & Expected Returns

To value the company, we started with management’s presentation to investors, dated June 18, 2024. In this presentation, KE provided a mid-term objective (2026 or 2027) of ¥330 billion in revenue, an operating margin of 30%+, and R&D spend of 6% of revenue or higher. We have built three forecast cases as follows:

Base case: We assume that management reaches their investor day revenue target, but in 2027. During that period, gross margins expand to 46.2% due to D&A and fixed cost leverage, while the company’s EBIT margin rises to 32.3% implying significant operating leverage. We note that SG&A (including R&D) rises 30% over this period. After 2027, we target LDD revenue growth, leading to a revenue CAGR of 19% over the entire forecast period. For context, the broader semiconductor market is expected to grow at 9% CAGR until 2030. We forecast further improvements in gross margins to 49.4% in 2029 based on further fixed cost and D&A leverage, and EBIT margins improving to ~35%. We note that these margins compare with ASML (GM – 51%, EBIT – 34%), another effective monopoly in the WFE market, and Disco Corp (GM – 70%, EBIT – 42%), a niche WFE supplier with a high-recurring stream of revenues.

Weak case: We assume that management does not hit their medium term target in 2027, but instead hits ¥315 billion in revenues in 2029 (95% of target), driven by delays in deployment of batch ALD equipment in 3D DRAM and GAA logic chips and market capture by single-wafer ALD toolmakers. We assume minor GM leverage (+70bps) despite revenue growth, and EBIT margins of 25.6% reflecting some operating leverage.

Best case: We assume that management grows revenues by 22.5% per year over the forecast period, mirroring similar growth as ASML experienced when lithography became the key-enabling technology of transistor shrink over the past decade. We forecast gross margins expanding to 54%, reflecting KE’s dominant position in batch ALD translating into material pricing power, and EBIT margins of 40% on revenues of ~US$3.3 billion. This reflects KE exploiting a defensible niche, similar to Disco and Lasertec (both with 40%+ EBIT margins).

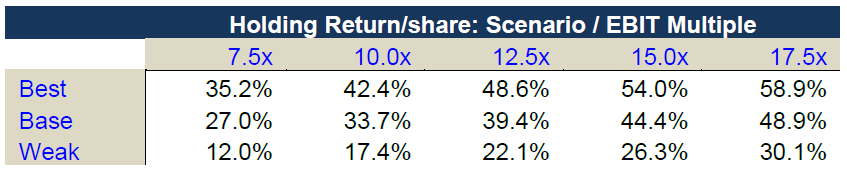

When using our base case assumptions along with a range of terminal EBIT multiples of 7.5 – 17.5x, we arrive at a discount to fair value of 40-60% at the current price of approximately ¥2,300 per share. Current prices imply a reasonable return even in the weak case scenario with a 7.5x terminal multiple, when KE trades at 14x 2024 EBIT and peers range from 16 – 30x.

Our estimated holding period return is 39% compounded to March 31, 2029, or a cash-on-cash return of 4.2x. Our weak case with a significant multiple derate to 7.5x implies a return of 12% compounded to 2029. Our sensitivity analysis of the expected returns compared to business case and exit multiples is provided below.

Finally, we summarize the drivers of expected return in our base case in the following waterfall chart. Interestingly, given the relatively low starting valuation, the forecasted cash generation alone would return 75% of the current share price.

Management and Execution Capabilities

Given the short period (~2 years) that the company has been a public company, it’s difficult to form a complete view on management’s execution capabilities and track record at achieving publicly stated targets. Additionally, there was a transition in senior leadership earlier in 2024, as three senior leaders stepped down as executive officers of KE to serve on the board, although the CEO remains in place.

The company also provides minimal information on its compensation structure and philosophy. However, the majority of stock-based compensation is attributed to options which are now exercisable as a public company. We expect that future equity-linked pay will continue to be in the form of options, providing some alignment between shareholders and the management team. We were not able to find evidence of any material holdings of the management team, or recent insider purchases, however.

Our surface level analysis concludes there is low alignment between management and shareholders at present. Management is also in a “show me” phase as they execute on their first round of external targets since becoming a publicly traded entity. Given KE’s technology leadership and existing customers wins with NAND chip manufacturers, we will give the team the benefit of the doubt in the interim but will be looking for signs of in-roads by Tokyo Electron in the segment. We also acknowledge that Japanese norms regarding management incentives and ownership may not be consistent with our own views formed by a North American perspective.

Governance and Shareholder Alignment

Currently, we can find no evidence of material economic alignment between the company’s board of directors and shareholders. KE’s board has eleven seats of which, three are occupied by the current management team, three are former members of the management team, and the remaining five independent directors come from diverse backgrounds, such as chemicals, law, and semiconductors.

The largest shareholders of KE are the private equity firm, KRR (~24% interest), and a strategic investor, Applied Materials (15%). Neither firm has a representative on KE’s board. As noted in the Executive Summary of this memo, KKR has been consistently reducing its interest in the company. At the time of the IPO in 2023, KKR held a 73% interest in the company, which decreased to 48% as a result of the public listing. In July 2024, when KKR announced plans to halve its economic stake by open market stock sales, its position had decreased to 43%[1], and most recent filing indicate KKR currently holds 24% (CapIQ). Given private equity fund lifetimes, we expect that KKR will continue to dispose of this position until it reaches zero, providing some overhang on the stock; the remaining position could represent any where from 10 to 20 days of total daily trading volume on the company’s stock, based on average daily volume over the past twelve months. Over the same period, AMAT’s interest in KE has been stable. We speculate that AMAT has maintained their ownership in KE to block a potential takeover of the company by a competitor and note that a senior VP from AMAT was a special guest at KE’s latest investor day.

Our overall view is that KE’s governance and incentive alignment leave much to be desired from a shareholder perspective. We would prefer board members to hold personally material economics interests in the company. We also find the lack of shareholder representation for AMAT in particular to be an interesting data point. We will remain on alert for any negative indications around shareholder alignment, particularly as KKR fully exits its position.

Further Research

While we have endeavoured to form a complete view on KE given the information available, we believe a couple of items of further due diligence are needed to gain full confidence in our recommendation. Specifically:

· Expert calls with deposition engineers in logic and DRAM to confirm KE’s technology advantage and understand the relative adoption rate and trends of batch vs single wafer ALD; we would also like to understand a timeline on further POR wins in DRAM and logic if possible.

· We would like to speak with management to understand the reason behind the observed low percentage of revenue allocated to R&D investment relative to peers. We also want to get a “feel” for management’s character, shareholder alignment, and capabilities, in light of the limited track record as a public company and low alignment with shareholders from an economic perspective.

[1] https://www.reuters.com/technology/kkr-cut-stake-japan-chip-tool-maker-kokusai-electric-sources-say-2024-07-09/